![]()

Advertiser Disclosure

Last update: November 17, 2024

5 minutes read

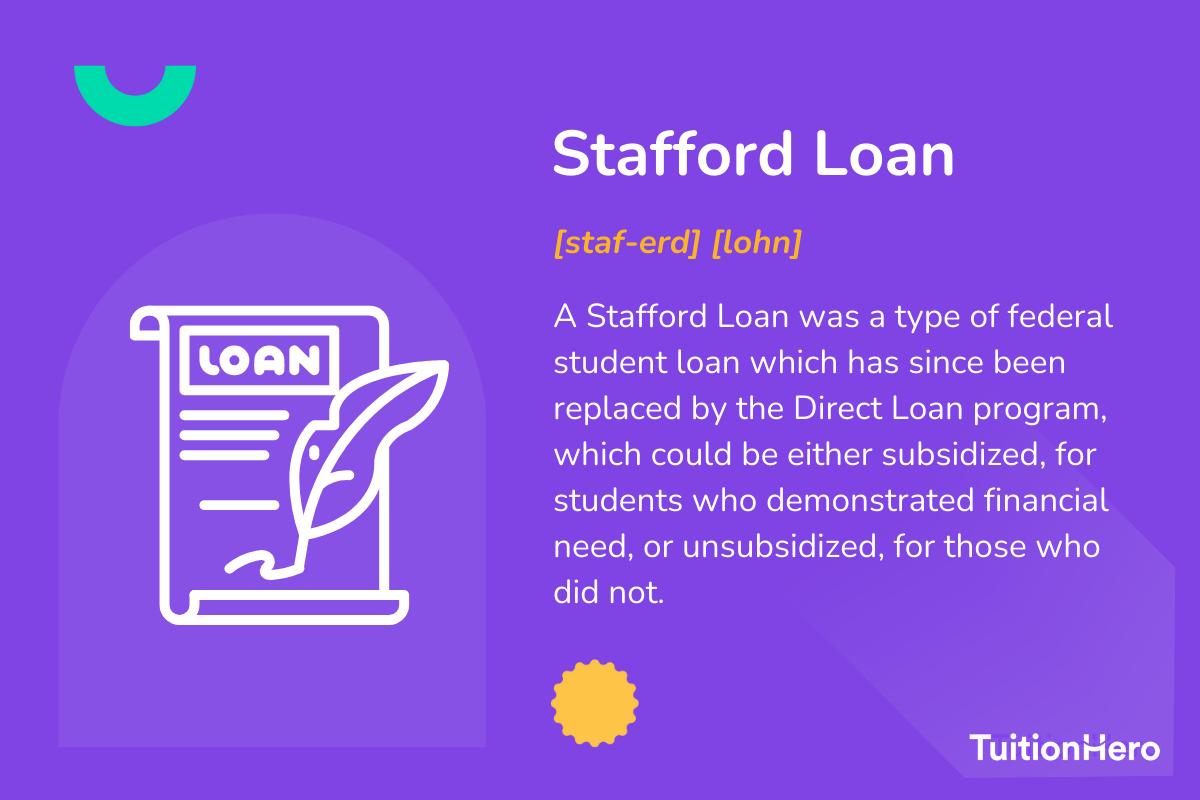

What is a Federal Stafford Loan?

Understand Stafford Loans their transition to direct loans, and manage your college debt effectively with our guide.

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

Have you been trying to figure out college finances and heard about Federal Stafford Loans? No worries, they're now called Federal Direct Loans. This post breaks down the basics of these loans, clears up common questions, and helps you handle your existing loans or look into other options.

Key takeaways

- Stafford Loans have been replaced by Federal Direct loans, but may still be part of your repayment portfolio

- Consolidating Stafford Loans can open up more repayment and forgiveness options, though with potential drawbacks

- Stafford Loans are not open for applications, but their successors, Direct Loans, are available via FAFSA

What is a Federal Stafford Loan?

A Federal Stafford Loan was one of the student loans offered by the government under the Federal Family Education Loan (FFEL) Program. But, after 2010, they stopped giving out these loans. Now, undergraduates can get Federal Direct loans instead.

How do I know if I have Federal Stafford Loans?

To find out if you have Federal Stafford Loans, you can follow these steps:

- Check with your loan servicer: Call the company that sends you bills for your student loans. You can find their contact info on the Federal Student Aid website or in letters you received.

- Check the National Student Loan Data System (NSLDS): Go to https://nsldsfap.ed.gov/ and log in with your Federal Student Aid (FSA) ID. This site shows all your federal student loans, including Stafford Loans.

- Review your award letter: Look at the letter your school sent you about financial aid. It should list the types and amounts of federal student loans, including Stafford Loans.

- Check your student loan documents: Look at any papers you got when you took out your student loans. They should say if you have Federal Stafford Loans.

- Contact your school’s financial aid office: If you're still not sure, call your school's financial aid office. They can help you understand what kinds of loans you have.

What repayment plans were available for Stafford Loans?

Stafford Loans came with a set of repayment strategies to fit different financial situations:

- Standard: Fixed payments over ten years.

- Graduated: Payments start lower and increase over time.

- Extended: Lower monthly payments, but over a longer period.

- Income-Based Repayment (IBR): Payments based on your income level.

TuitionHero Tip

A less common option, the Income-Sensitive Repayment Plan, depends on your earnings but is available only to low-income people. Contacting your loan servicer is the best way to explore this route.

Should I consolidate my Stafford Loans?

If you have an existing Stafford Loan, you should strongly consider consolidating it into a Direct Loan. Why?

First, consolidating combines multiple federal student loans into one, simplifying your life. Additionally, it can lock in a fixed interest rate at the average rate of all your loans rather than the variable rate common to Stafford loans.

Finally, consolidation can unlock additional Income-Driven Repayment (IDR) plans unique to direct loans, which might work better for your budget. But wait, before you decide to consolidate, make sure to check if you'd lose any borrower benefits. Stafford loans have almost identical benefits to the current Direct loan, but always make sure to confirm anyway.

Can I still apply for Stafford Loans?

Stafford Loans are still around, but they've got a new name: Direct Loans. When you're applying for federal student aid, just remember to go for Direct Loans instead of Stafford.

- Fill out your FAFSA to see if you qualify for Direct loans.

- Understand that FAFSA can also bring you grants, work-study, and scholarships.

- Be careful with private student loans because they don't have the same protections as federal loans.

How to consolidate and refinance your student loans

Both Stafford and Direct Loans can be streamlined under one roof with consolidation or refinancing. Consider these steps for a simplified financial process:

- List all your loans to get the full picture.

- Decide if federal loan protections or potential interest savings from private refinancing suit you best.

- Start the consolidation process via StudentAid.gov for federal loans.

- Shop around for the best refinance options if you're leaning towards private refinancing.

Check your college finance plan now and then to make sure it's the most affordable and simple option. For help with these tricky financial matters, TuitionHero has you covered. We help with everything from handling loans to finding the best scholarships.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

Dos and don'ts of managing Federal Stafford Loans

If you're paying back Stafford Loans or dealing with Federal Direct loans, it's important to be smart about it. Making the right moves and avoiding mistakes can save you money and stress in the long run.

Do

Consolidate for better terms

Keep track of your repayment plan

Explore income-driven repayment

Stay in touch with your loan servicer

Don't

Skip evaluating the pros and cons

Assume all repayment plans fit you

Miss out on potential forgiveness

Ignore notices or changes to your loans

Advantages and disadvantages of consolidating Stafford Loans

Consolidating your Stafford Loans can be a mixed bag. It might make repaying easier, or end up costing you more. The key is figuring out if the benefits outweigh the downsides and if it fits your financial plan.

- Grants access to more flexible repayment plans.

- May qualify for loan forgiveness programs.

- Simplifies finances by combining multiple loans into one.

- Interest capitalization might increase the amount owed.

- Possible extension of the repayment period, leading to more interest paid over time.

- You restart the clock on any progress toward forgiveness you might have made on existing loans, unless you apply to consolidate before April 30, 2024.

Why trust TuitionHero

At TuitionHero, we simplify college finance. We're here to guide you through loans, grants, and financial aid without confusion. Even though the Stafford Loan period is over, we're still here to assist. From Private Student Loans to FAFSA help, we've got your back in navigating education finances wisely.

Frequently asked questions (FAQ)

If you're combining your Stafford Loans into a Direct Consolidation Loan, you might qualify for PSLF. You’ll need to have a qualifying job, as well as make 120 eligible payments. To get all the details and check if you're doing things right, or if you want to apply for a Direct Consolidation Loan, visit StudentAid.gov for info or talk to us at TuitionHero for help.

If you have unconsolidated Stafford Loans, you can use the Income-Based Repayment (IBR) plan. But, if you consolidate, you get more choices, like Saving on a Valuable Education (SAVE)) or Pay As You Earn (PAYE). Figuring out which plan fits your financial situation is a bit like solving a puzzle. To learn more about repayment plans, check out our tips on income-driven repayment options at TuitionHero.

Sometimes things go off course, like missing a payment. First, take a breath. Then, quickly talk to your loan servicer - they’re the ones who handle your payments. They can help you figure out what to do and prevent any problems with your credit. You might get a break for a while, called forbearance or deferment, to give you time to fix things. Need tips on staying on track or catching up? TuitionHero can guide you to get things back on a smooth path.

Final thoughts

As we finish talking about Stafford Loans and federal student aid, remember to stay informed and take action. If you have Stafford Loans, know what choices you have.

If you're looking for new loans, learn about what's available now. Whether you're planning how to pay back loans or trying to get more funding, sites like TuitionHero can help you understand college finance and be more independent in your academic goals.

Source

Author

Brian Flaherty

Brian is a graduate of the University of Virginia where he earned a B.A. in Economics. After graduation, Brian spent four years working at a wealth management firm advising high-net-worth investors and institutions. During his time there, he passed the rigorous Series 65 exam and rose to a high-level strategy position.

Editor

Rachel Lauren

Rachel Lauren is the co-founder and COO of Debbie, a tech startup that offers an app to help people pay off their credit card debt for good through rewards and behavioral psychology. She was previously a venture capital investor at BDMI, as well as an equity research analyst at Credit Suisse.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

3 minutes read

Where Did Morgan Wallen Go to College? The Unexpected Path of a Country Star

Did Morgan Wallen go to college? See how a baseball injury changed his plans and how students can learn from his journey.

Learn More

5 minutes read

How to Build a Strong Resume for Internships

Wondering how to craft a compelling internship resume that grabs attention? Discover essential strategies to build a standout resume and secure your dream internship.

Learn More

8 minutes read

How to Get Your Student Loans Forgiven

Learn how to erase student loan debt with our top strategies for Public Service Loan Forgiveness, including employer tips and payment plans.

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today

Compare Personalized Rates